Creative Disruption

or: The Emerging Boom in the European Independent Sponsor Market.

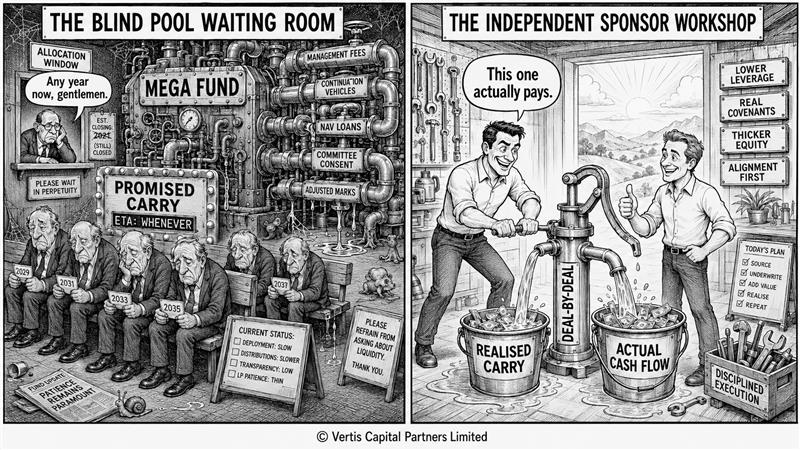

One of our heuristics is look what worked well over the last 10 years and consider the opposite. Private Equity worked exceptionally well but for reasons we will cover in a future VCO (hint: initial conditions matter), excess returns will be harder to come by in future. That puts pressure on the industry and creates opportunities to adapt and innovate. Big institutions will keep funding blind pools and mega-funds. After all a pension scheme looking to allocate $500 million into a diversified Private Equity portfolio needs scale and a brand name sponsor they trust. While that universe might be consolidating following four consecutive years of poor distributions and the slow correction of private market exuberance (aka the “Dodgeball Market”), there will be a place for experienced, high quality private equity funds that reliably deploy at scale.

Next to them sits an investor base with different demands. Family offices, sophisticated single LPs, wealthy individuals, a growing tier of endowments. They can afford to be selective. They want to understand the thesis before they write the cheque and for them the blind pool is less appealing. In search of alpha, they want to find deals that offer genuine value. Thankfully there is a growing number of enterprising private equity professionals who are leaving established funds to do just that. For them the appeal of deal-by-deal carry, eat-what-you-kill economics and the ability to truly focus on one or a handful of high-impact transactions with potentially life-changing outcomes is the pull away from established funds. Independent Sponsors (“IS”), often called fund-less sponsors, are one of the few “good news” corners of the European Private Equity market today and Vertis believes the IS ecosystem will continue to flourish in Europe. As the Dodgeball Market unfolds and carry hopes evaporate the switching costs for talent to ‘go it alone’ are decreasing. This movement is a good thing and will drive more investment into the Lower Mid-Market in Europe.

Vertis wants to support this ecosystem. We see the IS channel as one of the most attractive origination channels in European private credit today. This is driven by (typically) low purchase prices for the equity, less financial engineering (i.e. lower leverage), real covenants, and real cash equity investment alongside, in some instances, rolled founder/vendor equity. Just like LPs need to be careful which deal to pick so too must private credit players evaluate which independent sponsor to back.

In this issue we set out four things. First, the backdrop, i.e. the data behind the LP migration from blind-pool commitment, and the demand-side reallocation, including which LPs are active in this segment. Second, the supply-side talent migration that is now reshaping the European mid-market private equity landscape. Third, what this all means for credit providers, and fourth, we close with an in-depth conversation with Sullivan Street Partners alongside views from Calum Cusiter (Souter), Timo Hara (Certior Capital) and Edward Stubbings (Founder, Ternion and Global Emerging Manager Institute).

A note on intent: We write the Credit Observer to sharpen our own thinking and to hold ourselves accountable to the standards we set. We also use it to research trends and themes that are happening in the market. We welcome feedback and the debate.

The Backdrop: The Distribution Drought is now a Structural Condition

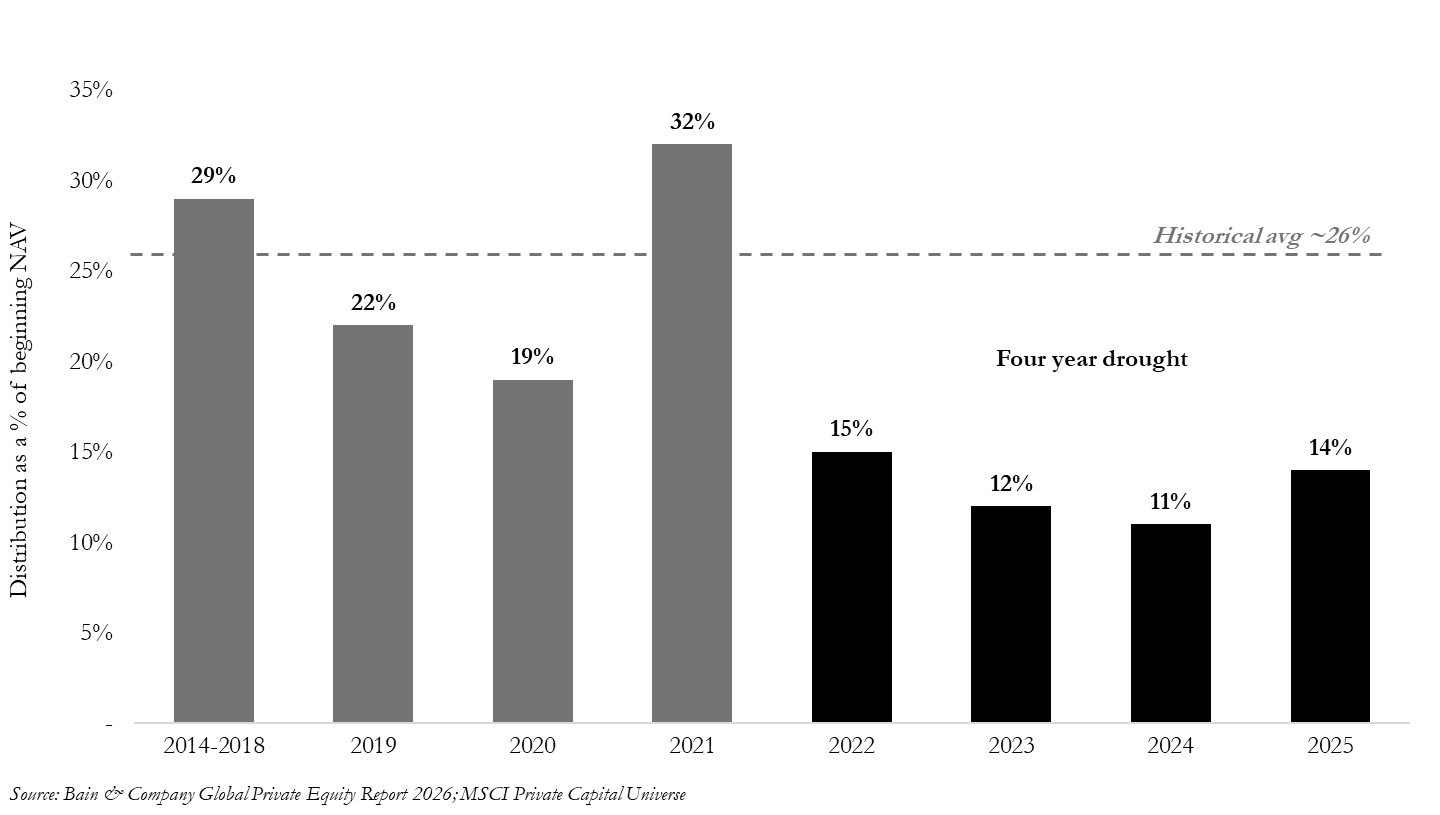

Bain’s 2026 Global Private Equity Report records that distributions as a percentage of beginning NAV remained essentially flat at 14% in 2025, a level last seen in 2008 and 2009. The metric has now trailed historical averages for four consecutive years. This includes the use of NAV lines and continuation vehicles, recent “innovations” which arguably flatter the numbers as further discussed below.

Global buyout funds are sitting on approximately $3.8tn in unrealised value across ~32,000 unsold portfolio companies. Average hold periods at exit have drifted to seven years, up from five to six years through 2010-2021 and even then exits are increasingly “manufactured” in non-traditional ways.

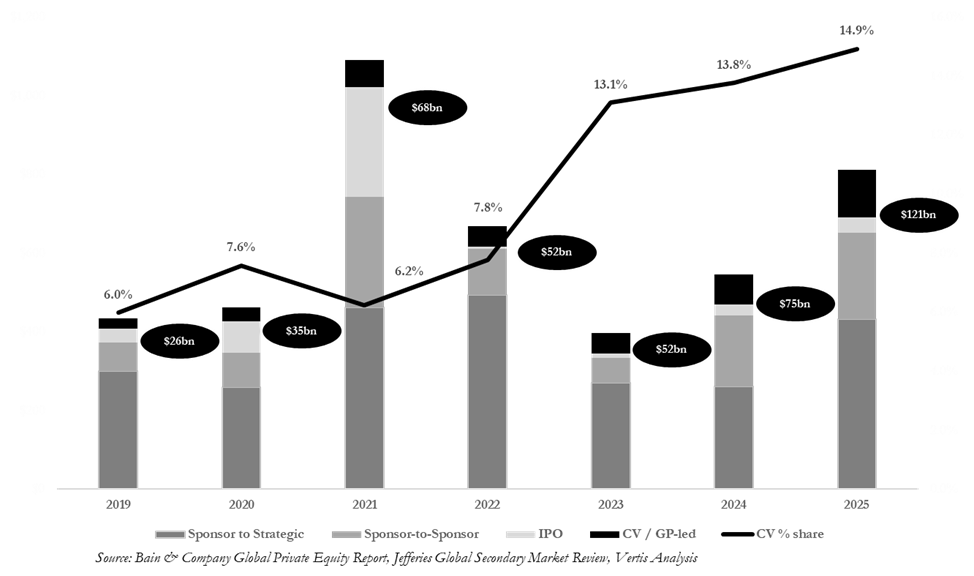

The industry has responded with financial engineering rather than distributions. Jefferies’ H1 2025 Global Secondary Market Review recorded a record $103bn of private equity stakes traded in the first half of 2025, up 51% year on year, with continuation vehicles accounting for roughly 19% of all sponsor-backed exits. NAV-based lending is projected by Oaktree and 17Capital to grow from $44bn in 2023 to $145bn by 2030.

Two underlying problems remain which will be future VCO topics: (1) average buyout valuations today are not conducive to attractive go-forward returns and (2) front-loading distributions and financial engineering pushes value realisation and recognition into the tail (the tail is where “surprises” live).

The LP reaction is now visible in the fundraising numbers. Buyout fundraising fell for a fourth consecutive year in 2025 with total capital raised down 16% to $395bn and the number of funds closed is down 23%. Even Tier 1 franchises are feeling it. Not all Tier 1 Sponsors will make it through this cycle and the universe of PE players will continue to consolidate at the top end. The ILPA LP Sentiment Survey reports more than half of LPs now believe they have more leverage with GPs than they did twelve months earlier.

The Independent Sponsor Model Offers Attractive Alternatives to the Traditional Blind Pool

Three structural complaints show up consistently across LP surveys from ILPA, Preqin, Coller and StepStone. First, the lack of DPI. The traditional PE model lives off capital velocity. Without cash returns, re-ups become conditional.

Second, alignment. In a traditional fund, carry is pooled across the portfolio. A single outsized winner can carry mediocre or underperforming deals on the GP’s side of the ledger while the LP absorbs the dispersion. Sector drift is a related effect. An LP signs up for a generalist buyout thesis in year one and finds the portfolio concentrated in a subsector by year three, with no deal-level veto. The first deal in a fund needs to be clean and easy to understand since you are fundraising with it. The last deal often does not get the same scrutiny.

Third, fee drag. Preqin reports average buyout management fees fell to 1.6% in 2025, down from the traditional 2%. That looks like a win for LPs but it is not the number that matters. What matters is absolute fees paid over the life of the fund. A blind pool charges on committed capital, then on invested capital, for ten years or more. Bain’s latest report shows that hold periods have drifted to seven years (or more) and funds run longer than they used to, so that meter runs longer too. An Independent Sponsor charges on deployed capital, on one deal, over three to four years on average. Run the arithmetic on a single transaction and the IS structure costs the LP less in absolute terms. The time period is shorter and it only runs on money at work.

The perception shift has not gone unnoticed by the LPs closest to the model. Christiaan de Lint, Managing Partner at Headway Capital Partners, captured it in their 2025 white paper: “Ten years ago, people questioned why you would want to back a team that couldn’t raise a fund. After recent liquidity and fundraising challenges, investors are now understanding that the Independent Sponsor model is not only poised for tremendous growth but is here to stay because some of the best private equity professionals have adopted it.”

The Demand Side: Who is Reallocating, and Why?

LPs who used to take pan-European LMM exposure through committed funds now buy it three ways. A smaller core of high-conviction blind-pool re-ups. A growing slice of co-investment. A deliberate, deal-by-deal allocation to Independent Sponsors. The third bucket is growing fastest. LPs are driving it.

Family offices are leading the way. J.P. Morgan’s 2026 Global Family Office Report, covering 333 family offices across 30 countries, finds half of them plan to execute direct deals through Independent Sponsors. Club deals make up roughly 60% of family-office direct investment volume. Citi’s 2025 report finds 70% of family offices now do direct investing. BNY’s 2025 SFO Insights records 64% of single family offices expecting six or more direct investments in 2026, a 52% jump year on year, with alignment of interests cited as the main reason. Family offices already supply roughly 62% of US IS capital. The European pool is thinner but growing quickly. US endowments and foundations are entering through the dedicated fund-of-funds tier. TIFF Investment Management’s late-2025 paper, Ten Observations on the Independent Sponsor Market, calls this out as a structural reallocation. Pension funds mostly access the IS market indirectly, through Headway, Keyhaven, Pantheon and the other FoF players.

Three behavioural shifts sit underneath the data.

First, co-investment fatigue is real. The fee-saving rationale of co-invest has lost some of its shine. Deal flow is dominated by mega-fund GPs offering larger, more competitive “franchise” transactions. LPs lack the staffing to underwrite tight-clock deals. Exposures end up concentrated by vintage and sector. IS deal-by-deal access solves the selection (off-market / proprietary), alignment and DPI problems at once, with sponsors whose whole reputation rides on every transaction. At the end of the day it’s about performance. If initial conditions dominate and average PE valuations for “franchise” transactions remain elevated, well-picked IS deal have significant room to outperform.

Second, asset-first underwriting workflow is genuinely different. In a blind pool, the LP underwrites a team and a strategy. In an IS deal, the LP underwrites a team, a strategy and the actual asset before committing a pound. Family offices think about direct equity investments the same way.

Third, the dedicated IS fund-of-funds tier has institutionalised access. For LPs who want IS exposure but not the operational burden of running a deal-by-deal programme, the European backbone now exists at scale: Headway Capital Partners (London/Boston, founded 2004; HIP V closed at €627m in May 2024 against a €500m target; >€1bn AUM and 140+ transactions with 100+ IS or GPs); Keyhaven Capital Partners (London, 2003; >€2.2bn invested across 65+ direct and secondary transactions in the European LMM); Souter Investments (Edinburgh, the Brian Souter family office: >£750m across 100+ unquoted businesses, current portfolio over £400m); Opera Investment Partners (Zurich, 2020; >€400m committed); Yana Investment Partners (London/Vienna, 2017); Clearsight Investments (Pfäffikon, 2008); Maxus Capital (Ghent/London, 2022). The capital ecosystem that used to be Headway plus a handful of family offices has deepened.

Edward Stubbings, founder of the Global Emerging Manager Institute and Ternion, has tracked this evolution for years. He points to the historical bottleneck: “One of the limiting factors to the growth of the independent sponsor ecosystem was historically the lack of LP capital. Co-invest pools were still holding out for fee and carry-free opportunities, and family offices were tough to find. This has now changed. Our Global Emerging Manager Institute is one of a few places that has sought to track the now many active investors in independent sponsor deals globally.”

The data is clear. Bain and ILPA find 63% of LPs prefer a conventional exit at a lower valuation over a dividend recap or continuation vehicle. They want realisations, not financial engineering. Coller’s 42nd Barometer finds 38% of LPs expect new manager formation to outpace consolidation, and 36% report seeing more spinouts in their portfolios in the past two to three years. The marginal LP dollar is being re-routed to deal-by-deal exposure where the asset, the sponsor and the alignment get underwritten in a single decision.

The line that captures it comes from an Addleshaw Goddard partner, echoing the FT in 2025: “Barely a conversation goes by with investors who aren’t looking at, or are open to, doing deal-by-deal type investments.”

Timo Hara, Founding Partner at Certior Capital, highlights the importance of creating value on the buy. Certior Capital is a European fund-of-funds that allocates capital to emerging managers and Independent Sponsors, and they have seen enough of the universe to think hard about what makes a credible sponsor. “For us, one of the key themes within the Independent Sponsor model is the ability to match the right buyer with the right asset. This means the buyer should have a compelling reason to ‘win’ the deal, beyond simply offering the highest price. That reason may be sector or operational expertise, or the ability to convince a re-investing vendor that they can deliver the most value during the next phase of ownership. Equally, it could be the strength of their network, personal chemistry, cultural alignment, or a willingness to go the extra mile to better understand a misunderstood or complex asset. Whatever the reason, within our sponsor underwriting, we need to build conviction not only that the sponsor is sufficiently qualified, but also that they are winning the asset for the right reasons.”

That last sentence is critical. The question ‘does this sponsor have the right to win’ is the discipline that lenders should apply too.

The Talent is Voting with its Feet

The LP critique explains the demand side. It does not explain why the supply of Independent Sponsors has doubled in two years. For that, look at the incentive map inside mega-funds.

A Principal who joined a $15bn flagship in 2019 is seven years in. The 2019 fund is deploying its last remaining capital. The 2022 fund is 40% invested and underwater. Carry on the 2019 vehicle is theoretical until 2028 at the earliest, subject to continuation vehicles, NAV loans and whatever the GP does with the tail. The math of waiting is unforgiving; where a share of carry in a pooled $15bn fund, diluted across ~25 partners, held hostage to a handful of $1bn deals that must clear hurdle, discounted back across the hold period. The expected value has collapsed.

Now the Principal who left in 2021 to do deal-by-deal. Three platform deals closed. Average equity cheque £15m. Average entry multiple 6x. One exit at 4.2x MOIC in year three. Carry paid in cash. Two deals still running, marked conservatively, with founder/vendor rollover, real alignment from the outset, and real financial covenants to adhere to. Given disciplined entry points and valuation metrics, healthy returns are achievable (not aspirational). On a smaller base, the economics already beat what the former colleague will see from the 2019 mega-fund on any reasonable scenario.

The point is obvious once you say it. Do good deals. Buy value, realise profits, return capital. The money follows. Initial conditions dominate and they are good in the LMM and they are not good in the broader LBO market. Buy at the average valuation today, on a franchise deal, at mega-fund leverage, and it will be a struggle to create value for your LPs or for yourself. Add that even when you do find the good deal inside a mega-fund, your personal carry is so diluted, and the fund’s performance so hostage to whatever the rest of the partnership does, that the math barely moves for you.

This is creative disruption running through private equity the way it ran through every industry with bloated incumbents and mispriced labour. The mega-fund model sold a generational bargain. Grind for a decade, wait for carry, get rich. The up and coming talent is doing the math. And for many of them it is no longer adding up.

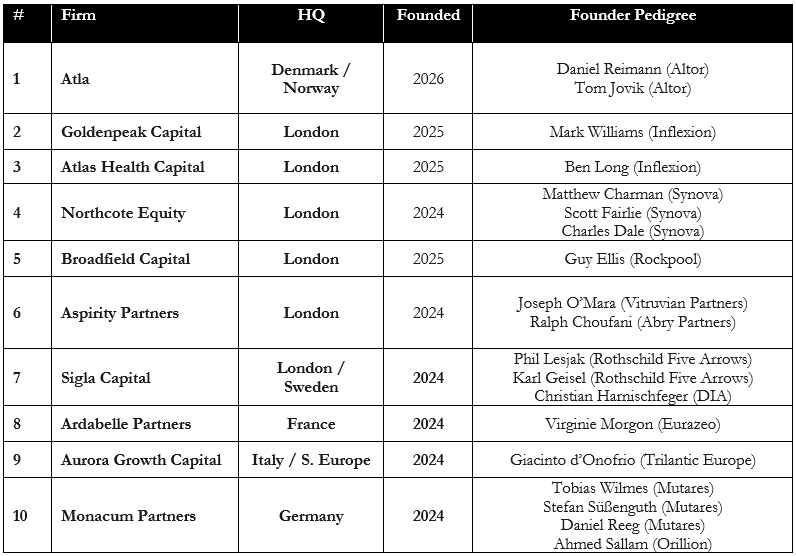

In the last five years, a generation of European mid-market PE professionals have walked out of established platforms to set up deal-by-deal vehicles. Some have stayed deal-by-deal. Some have used the IS track record to raise a first institutional fund.

The provenance pattern is unmistakable: Altor, Inflexion, Synova, Vitruvian, Abry, Eurazeo, Mutares, Trilantic. Goldenpeak raising £375m in roughly 12 weeks against demand well above target, and Northcote raising £160m in 16 weeks at a hard cap against demand above £300m, are not anomalies. The Headway 2025 white paper finds that more than 70% of European Independent Sponsors plan to remain fund-less long-term. What used to be a stepping stone has become a viable destination.

The mega-funds will keep their elite tier. The largest, best-performing franchises will keep raising and deploying. Our point is narrower. For the mid-tier platforms, for the Principals and MDs one or two rungs below Partner, for the Lower Mid-Market deal opportunity across Europe, the Independent Sponsor model is coming into its own.

Strip away the novelty and this is an old structure returning. Capital-light, principal-led, syndicated deal-by-deal to a network of trusted co-investors, your neck and reputation always firmly on the line. That is merchant banking. Independent sponsoring is the merchant banking model returning under a modern compliance regime. The same unbundling already ran through hedge funds in the 1990s and through the boutique investment banks in the 2010s. Private equity is the last of the three to go.

Independent Sponsors: Where Demand and Supply Meet

An Independent Sponsor identifies, diligences and signs a deal first, then raises the equity per transaction from a curated roster of LPs. The economics are deal-specific: a closing fee, usually 1% to 1.5% of enterprise value in Europe per the Addleshaw Goddard 2025 Independent Sponsor Deal Terms Survey, a management fee, and carry tied to that deal’s outcome, most often 15% to 20%, with tiered hurdles becoming standard. The LP sees the asset before committing. The GP eats what it kills.

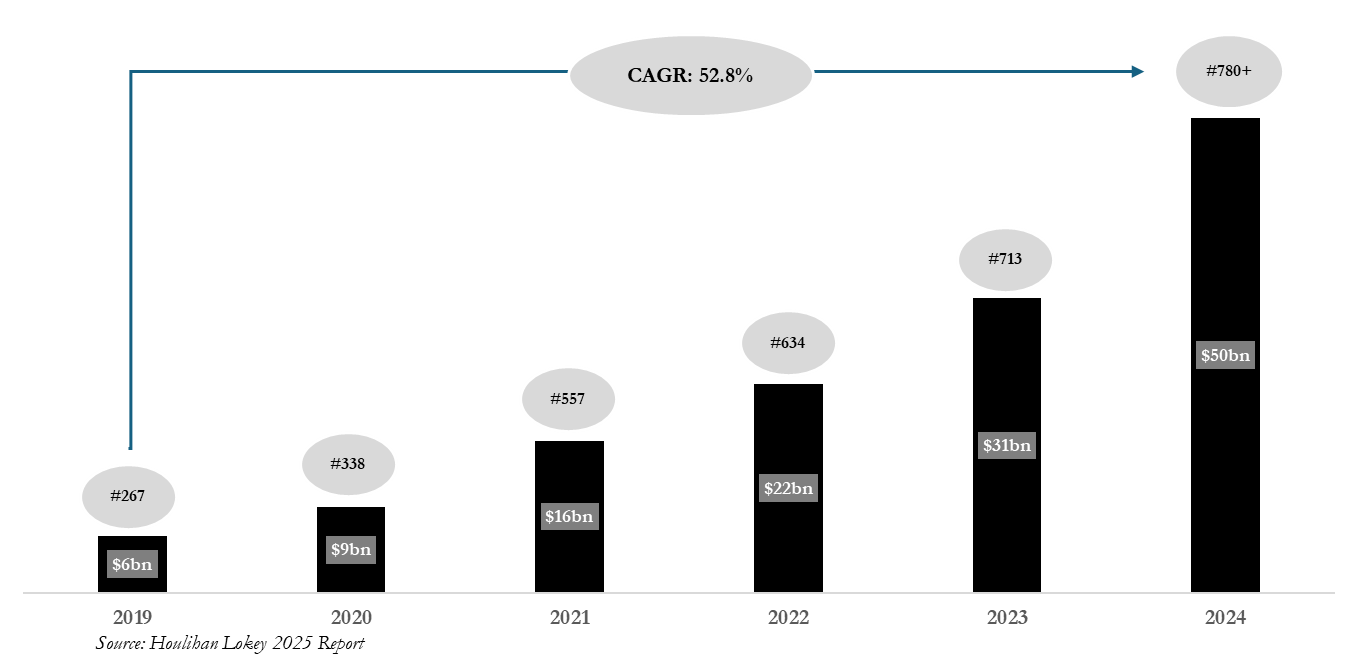

The Addleshaw Goddard 2025 Survey records well over 500 Independent Sponsors active across Europe, with new entrants every month. Headway's 2025 white paper, “Inside the Independent Sponsor Market”, reports the surveyed IS community alone expects to deploy roughly $8bn in 2026, and that over 70% plan to stay fund-less long-term rather than treat IS as a stepping stone. Houlihan Lokey estimates global IS transaction volume has more than doubled since 2023. That doubling tracks the departure curve out of upper mid-market and mega-fund platforms, not just LP reallocation.

The Performance Arithmetic Favours the Model

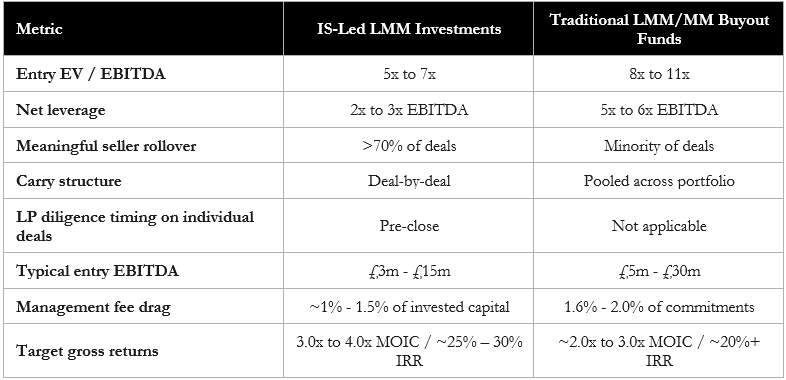

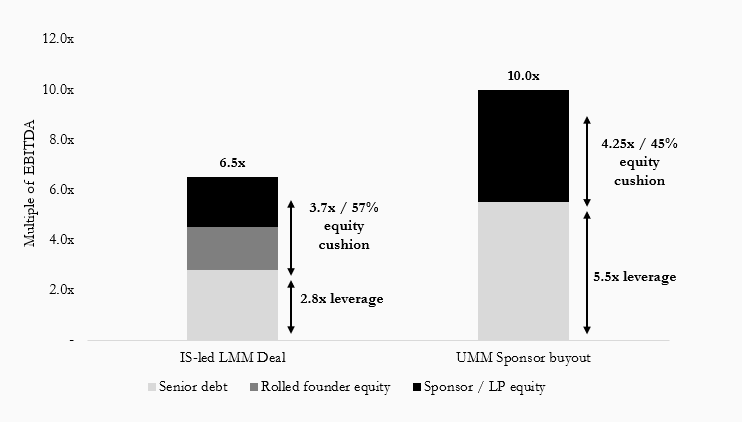

Independent Sponsor deals sit where Lower Mid-Market value is created. Founder-owned businesses, smaller carve-outs and complex situations below the radar of mega-funds. The Addleshaw Goddard 2025 Survey of transactions completed in 2023 and 2024 shows the most common number of equity investors in a European IS deal is one. The typical initial debt-to-equity ratio is 1:1, implying opening net leverage around 2.0x to 3.0x EBITDA. That compares to ~5x to 6x in traditional sponsor buyouts of scale across the mid and upper mid-market. Entry multiples cluster around 5x to 7x EV/EBITDA, below broader LMM and MM averages. Seller rollover is a structural feature where founder equity stays in the deal in most transactions (often subordinated) and that gives an implied and actual equity cushion that institutional buyouts rarely match.

Dedicated IS backers target 3.0x to 4.0x MOIC and 25% to 30% gross IRRs on their deal-by-deal portfolios. Realised exits skew above 2.5x with a meaningful tail above 4.0x MOIC per Headway’s 2025 survey. The numbers are achievable because the IS model forces selection quality on every transaction. There is nowhere for a marginal transaction to hide inside a pool average. The point is not how many opportunities a sponsor reviews. The point is whether the sponsor wins the right one for the right reasons.

Why European Independent Sponsors are Having a Moment

Europe’s fragmentation is usually cited as a reason to prefer pan-regional mega-funds. We will make the opposite point. Fragmentation is why Independent Sponsors are better placed to harvest the coming wave of Lower Mid-Market succession opportunities. The European LMM is not one market. It is seven or eight national markets separated by language, law, accounting convention, banking relationships and management culture. A founder selling a €12m EBITDA Mittelstand business runs a German-language auction through a regional M&A boutique, under German law, with bidders who navigate works council consultation rights from day one. A founder selling an €8m EBITDA French insurance broker runs an entirely different process through an entirely different network. Sourcing takes local relationships, local language and local credibility, and that is uneconomic to maintain at mega-fund scale at this end of the market.

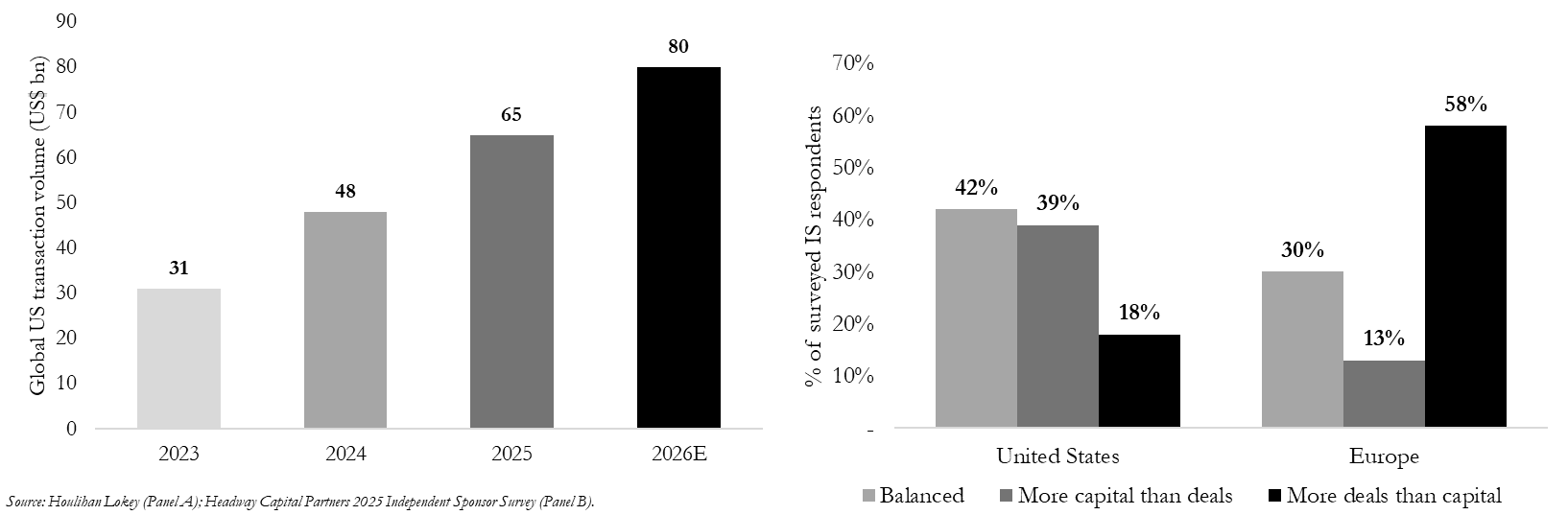

The Independent Sponsor model fits this terrain. A small team can specialise nationally or sub-sectorally, build relationships, do deals, and avoid costly overhead. Europe’s family-owned business cohort is entering a multi-year generational transition, with thousands of founder-led Mittelstand, Benelux and UK SME businesses facing succession decisions through 2030. Capital supply inside Europe has not kept pace. Headway’s 2025 survey found 58% of European respondents see more deal volume than available capital, versus only 13% of US respondents reporting the same imbalance. Europe is, on this measure, the structurally capital-short IS market.

The IS model fits a particular kind of European transaction. Carve-outs from larger groups. Founder-led businesses with messy capital structures. Cross-border situations where the asset’s true value is hidden inside legal, accounting or operational complexity. Well invested but slow-growing legacy assets with cost-cutting potential. These are not deals that move through auctions in three weeks. The IS fundraising timeline, often presented as a weakness, is a feature here. Weeks spent assembling the LP roster are weeks spent understanding the asset. The vendor sees the buyer stick with the complexity. If the deal holds up through that process, both sides know they have the right pairing.

The same logic applies even more forcefully in regulated financial services. Insurance, asset management, payments, lending, banking. These are categories where regulatory permission often is a structural moat and where the traditional blind-pool model and now faces direct scrutiny from the regulator itself. For the insurance industry specifically, the European regulator’s (EIOPA) January 2026 Consultation Paper makes the point explicit. The question is no longer just whether the buyer is qualified. The question is whether the fund structure itself is compatible with the long-term obligations of a regulated insurer. The four concerns EIOPA flagged read like a description of the closed-end fund: a short investment horizon misaligned with multi-decade policyholder liabilities, complex multi-layered acquisition vehicles, pressure for short-term value extraction, and aggressive asset reallocation post-acquisition. National supervisors have already begun acting on the same view. Approvals for short-horizon PE acquirers of European life books have effectively closed. Several recent transactions have been pulled, restructured, or sold on to alternative ownership structures.

The €3.5 billion sale of Viridium last year is the canonical example of where the market has landed. Germany’s largest closed-life consolidator was transferred from a PE fund owner structure, following the insolvency of a separate insurer owned by the same PE fund in Italy, to a consortium of Allianz, BlackRock, Generali, T&D Holdings, Santander Insurance and a family office. The transaction is the template for how regulated FS ownership now has to look.

The Independent Sponsor model sits naturally inside that template across a complex and regulated financial services sector. Permanent or deal-by-deal capital with aligned holding periods. Transparent ownership. Operator-investors who have run the businesses they now back. Direct accountability to a small, named investor base rather than diffuse fund-of-fund chains. Majority or minority investments. Public or privately held business. Flexibility is increasingly key. Our sister company Henry Costa Partners is built exactly on this thesis. A merchant banking platform for European regulated financial services, often working in close partnership with some of the leading strategic players in the industry. The right to win in regulated financial services comes from operator credibility, regulatory fluency, and an investor roster the regulator and the counterparty both recognise.

The LP control argument resonates particularly with LPs who have been disappointed by fund managers’ ability to lean into the cycle when the time is right. Calum Cusiter, Managing Director at Souter Investments, illustrates it plainly: “The biggest pull of the independent sponsor model is control over our own capital, particularly timing and the exposure we get to each specific deal: commit to a blind pool and you have no idea when it gets drawn and what it is invested in. When we were not as focussed on direct PE as our current strategy, we committed to a distressed fund early in the GFC because the cycle was right; by the time the capital deployed five years later, the opportunity was gone. The deal-by-deal model lets us think about individual structures, valuations and sectors, where a fund is generic by design.”

Lending to Independent Sponsors is Good Credit

For a disciplined credit manager, the IS borrower is one of the most attractive risk-adjusted propositions in the European LMM. Leverage is lower, 2x to 3x opening net leverage against 4x and up in parts of the LMM and 5x and up in the upper mid-market. Default probability falls. Loss-given-default falls further, because the equity cushion is thicker and usually includes rolled seller equity aligned with operational continuity. Covenants are real, no cov-lite. Diligence access is closer to direct-lender-to-corporate than sponsor-gated, because the IS has neither the incentive nor the standing relationships to run a lender-unfriendly process. Lender influence is higher, because the lender has genuine information rights and a smaller, more accountable sponsor on the other side.

Private equity and private credit are going through choppy waters. Our thesis is during these times “old school” credit underwriting wins. Hence our focus on lower leverage, real covenants and downside protection. That’s what drives us to the Lower Mid-Market. We are not chasing the upper mid-market sponsor franchise that so much of the private credit industry continues to compete for. It is in the fragmented, disciplined, structurally capital-short European LMM where we see great opportunities. Supporting the IS ecosystem is an important part of that.

There is a less obvious feature of the IS model that benefits the lender as much as the LP. The IS roster on a typical deal is not a passive cap table. Many of the LPs are retired PE professionals, sector operators, former CFOs, and family offices with operating company experience. They underwrite the deal alongside the sponsor. They challenge the thesis. They flag the questions the sponsor missed. In effect, every IS transaction has a crowd-sourced investment committee built into the equity stack. A lender underwriting alongside this structure is underwriting alongside more relevant brainpower than is often assembled around a blind-pool transaction at this end of the market.

DunPort, our strategic partner, has deployed over €1.4bn across the Lower Mid-Market since inception in 2017, with the same discipline around covenants, structure and capital preservation that we set out in our January issue. To date, DunPort has backed 12 IS transactions, deploying €197.6m cumulative capital. Ross Morrow Founder of DunPort puts the underwriting case clearly: “Our core principle is simple: return of capital first, return on capital second. In IS-led transactions, lenders’ economics are often more attractive, they can more actively conduct their own due diligence, and they are able to exert greater influence over portfolio companies.”

The obvious objection when backing IS-led transactions is the absence of a committed fund. When a company underperforms, a blind pool GP has reserves. An Independent Sponsor does not. Unless capital was committed for the deal at close, which is the exception not the rule, there is no dry powder behind it. A lender has to take that seriously, and we do.

But the binary is misleading. Lower entry leverage means pressure arrives later and equity value still exists at the point of theoretical enforcement. We discussed this in detail in the DunPort / Vertis White Paper referenced in VCO #1. Rolled founder equity keeps the person who knows the business best in the deal and motivated to fix it. Follow-on capital is assembled rather than reserved. Some LPs ring-fence amounts informally on their own side. The sponsor's job is to bring the same recommendation to the LP roster that any GP would bring to its investment committee: good money after good, not good money after bad. The honest part is that speed and certainty are lower than a funded GP offers. That is exactly why sponsor selection matters more here, not less. Lenders should ask this question on every investment, and the only answer that holds up is a track record of following money when the asset deserved it, and walking when it did not.

And eyes wide open: an Independent Sponsor acts rationally on a single deal. A GP may have an incentive to keep a marginal asset alive, because not doing so might drag the fund below the carry hurdle for the entire pool. The decision would not hold up against the best alternative use of that capital. The fund-level math makes it rational anyway. An Independent Sponsor has no pool to worry about. The carry is on this deal, so the follow-on decision is made on the deal. They support the asset when it deserves support and walk when it does not.

EIGHT QUESTIONS FOR: SULLIVAN STREET PARTNERS

A London-based Independent Sponsor, focused on complex situations in the UK Lower Mid-Market.

Sullivan Street Partners was founded in 2010 and is led by Managing Partners Layton Tamberlin (prev. TDR) and Zeina Bain (prev. Carlyle Group and ICG). Sullivan Street invests £30m to £75m of equity per transaction, acquiring controlling stakes in fundamentally strong businesses where carve-outs, operational change or structural/esoteric complexity create opportunities for conviction-led, hands-on ownership. Recent activity includes the July 2025 acquisition of Senior plc’s Aerostructures business for up to £200m (rebranded Zenix Aerospace and backed by Headway Investment Partners V, alongside Keyhaven Capital Partners and others) as well as UKAT, Zelus and the Ancora Group, alongside the exits of Octavius Infrastructure to RSK in 2025 and Tivoli to Nurture Group in 2024. Sullivan Street was named Independent Sponsor of the Year at the 2025 Mergermarket British Private Equity Awards.

We are speaking to Oliver Marshall, Partner at Sullivan Street, who has been with the business for over 10 years.

Vertis: Sullivan Street has now been running the Independent Sponsor model for fifteen years. What do LPs most often get wrong about it?

Marshall: “The LPs we deal with day to day understand the model and like it; institutionalised family offices and groups like Headway are specifically looking for managers like us. The friction tends to come from institutional LPs that have grown up investing in blind pools. They are increasingly attracted to deal-by-deal investing because they value the visibility, shorter duration and direct alignment with motivated managers on each transaction. However, because they are newer to the model, they can sometimes instinctively view these opportunities as co-investments and resist paying fees. That is really an education point. This is not co-investment alongside a fund where management fees have already been paid on committed capital. There is no committed blind-pool capital here; we are paid on deployed capital, with carry as the main incentive. Ultimately, the fees are better than blind pools as there is no fee drag on committed but unspent but it is important that there is alignment in the economics to drive win-win outcomes.”

Vertis: The standard lender objection to independent sponsor transactions is the absence of a committed fund. When a portfolio company hits a covenant breach, a liquidity squeeze or a capital structure reset, what is the playbook?

Marshall: “Generally speaking we do not usually take hard future commitments from LPs at close, and we do not pretend otherwise. Some LPs ring-fence amounts informally on their own side, but that is up to them. When follow-on capital is needed, whether for M&A, growth, liquidity, covenant cures or a wholesale capital structure reset, we go back to the LPs with a recommendation. The test is the same one we applied at entry: good money after good, or good money after bad. In every situation we have faced, LPs have followed our advice in both directions. In that sense for lenders the key issue – will a GP actually want to follow their money – is the same for us as for a fund. Just because a blind fund GP has committed capital does not mean they will always think it sensible to follow their money – this always gets lost in those conversations.

Lenders do however ask this question on all of our deals. Our answer is our track record. It is also why manager selection matters so much in independent sponsor transactions.”

Vertis: You have started using a Short Duration Vehicle structure. Please walk us through it.

Marshall: “Over the last 18 months, we have moved to a more structured form of financing, which is essentially a three-deal fund; we call it a Short Duration Vehicle, or SDV. Our prior three deals went through this structure. The LPs underwrite and close on the first deal, have visibility on the second, and accept a third blind allocation governed by a tight buy-box: EBITDA range, sector, valuation, margin profile. We can then bring-in other co-investors from our network on top of the SDV to flex with deal size.

We have had a lot of interest in this structure as it gives the LP shorter gestation, visibility on assets and themes, and scalability. The driver for us is actually not the committed capital of the third – we are very comfortable with our ability to raise money from our investors deal by deal, our history speaks for itself. The real attraction is honestly the ability to pursue more opportunities concurrently, as fundraising is a time drag at a senior level, and reducing that time commitment by up to a third makes an enormous difference to our available time as a team.

We are on our second SDV vintage now. Mi Hub, a provider of bespoke and technical uniforms for businesses, was the first investment in it. A TMT buy-out is expected to close shortly, with the blind allocation to follow.”

Vertis: Sullivan Street writes equity cheques of £30m to £75m. How has the European capital provider ecosystem evolved, and where are the gaps?

Marshall: “We are established now. Our LP network ranges from smaller HNW to tickets of up to £50m from the larger fund-of-funds. Because of this when we have a differentiated opportunity, we can assemble the cheque quickly. The harder path is the new manager assembling those cheque sizes without pre-existing relationships. That is why so many emerging Independent Sponsors start with buy-and-build: you start small, do the platform, and use secondary raises to attract more capital alongside the demonstrated track record.

That said, the evolution of the independent sponsor market over the last decade has been remarkable. The depth, sophistication and liquidity of the LP network has changed materially. Ten years ago, raising meaningful institutional capital on a deal-by-deal basis was much harder and the investor base was narrower. Today, there is a far more developed ecosystem of fund-of-funds, family offices, institutionalised private capital groups and specialist investors who understand the model and are actively looking for access to high-quality independent sponsors. That liquidity has been a major driver of the growth and institutionalisation of the market.”

Vertis: Europe versus US on capital availability.

Marshall: “The US is a more mature private equity market. Search funds, independent sponsors, and deal-by-deal investing have all been around for longer so there is more liquidity, a deeper capital base and a more developed ecosystem. but that also brings more competition, more process intensity and, ultimately, higher prices.

Europe is earlier in that evolution. The opportunity set is more variegated, but the capital is more fragmented. Our LP base is genuinely mixed: UK, US and European, all aligned around the strategy and the specific opportunity rather than geography alone. There is a lot of capital in Europe but it sits in much less visible pockets, so relationships matter. Placement agents can be useful in this market in much the same way they are for blind-pool fundraising.

US LP interest in European opportunities has increased materially over the last couple of years. Part of that reflects the growing maturity of the independent sponsor model, but it is also driven by the relative asymmetry in valuation multiples. In the US, many sectors and processes have become highly competitive and increasingly commoditised. Europe can still offer opportunities to back high-quality businesses at more attractive entry points, particularly where there is complexity, disintermediation, fragmentation or a need for hands-on ownership. Before this recent shift, many US LPs were much more focused on their home market.”

Vertis: What do credit investors typically get wrong on Independent Sponsor deals, and what do you look for in a lender?

Marshall: “We value-driven investors are looking to generate asymmetric returns. Given deal complexity, cost of capital is therefore not our primary focus, but that is not licence for lenders to charge what they like. What we need is certainty and flexibility. We are often looking at storied credits that need a bit more unpacking: carve-outs, complex buyouts and situations with noise. The lender has to understand the underlying business, look through the contextual issues and back the conviction we have built through our diligence. They also have to ride the journey of the process with us, because these transactions are rarely linear.

Lenders often focus too much on the absence of a committed blind pool rather than the actual sponsor, LP base and track record. The right question is not simply whether there is committed fund capital behind the deal; it is how the sponsor has behaved when follow-on capital has been required, whether LPs have supported the recommendation, and whether there is a long-standing, loyal partnership between the sponsor and its investors. The answer comes from case studies, track record and evidence of having done it before.”

Vertis: The 2025 Headway Report says 58% of European Independent Sponsors see more deal volume than available capital, against 13% in the US. Does that match your experience?

Marshall: “There are always plenty of deals. But it’s is not simply deal volume versus available capital, but the match between sponsor quality, the quality of the opportunity and the right LP base. We definitely do not see more deals that we want to execute than we see available capital – capital has never been a problem for us – but it is difficult to comment on how that would work for the deal market as a whole. Strong managers with differentiated opportunities can still raise capital, but the bar is high and the process is relationship-driven. Equally we are highly selective in our deals. So the reason for us finding balance could be either, both or neither of these reasons

People running around the market with one-off deals will struggle if they do not have established LP relationships, because LPs generally need to see multiple opportunities and build trust before they back a manager. In that sense, capital availability is not binary. There is capital for good deals and credible sponsors, but it is much harder to access if you are starting from a standing start. You have to build the first relationship and prove the first deal before you can scale into the rest. This may be a statistic where the respondents are coloured by the deals they showed – just because capital is not available for a particular deal doesn’t mean it isn’t available, it just might not be a good deal!”

Vertis: Headway also reports 70% of Independent Sponsors intend to remain fund-less. Where does Sullivan Street sit, and would you ever raise a traditional blind pool?

Marshall: “In this fundraising market I am surprised it is not 100% - nobody wants to say they will and then fail do they! I wouldn’t necessarily say the traditional blind pool is dead, but it is much harder than it used to be unless you are a top-performing, established manager with the track record and institutional infrastructure to support it. LP appetite has become more selective, and many investors now want greater visibility, shorter duration and more direct alignment with specific opportunities.

In terms of Sullivan Street, never say never, but we are not currently even thinking raising a traditional blind pool, because we do not want to tie the strategy to artificial deployment pressure or overly rigid fund restrictions. Our strategy is opportunity-led and conviction-led. It needs flexibility from LPs, and that aligns much better with deal-by-deal capital and with our SDV structure. We also have to be cognisant of the fact that we have been operating in this way for 16 years, evolved as a firm around this model, and proven ourselves to be very good at it. Blind pool investing is different – who is to say if we would replicate this success or find friction in a change of model. At this moment in time we certainly don’t want to mess with a successful recipe.”

Vertis: Thank you Oli and Sullivan Street.

At Vertis we are building the leading credit platform for Europe’s Lower Mid-Market. We are doing this across cash-flow lending via our strategic partnership with DunPort Capital Management and asset-backed lending via Vertis Capital Solutions.

Published by the Investment Team at Vertis.