THE DODGEBALL MARKET

Or: Why initial conditions dominate.

When markets are overvalued and “adjusted” numbers flatter reality, fragility creeps in. In 2025 we started to see some initial signs of anxiety creeping into the private credit market.

Our base case is a long grind through private market marks and valuations, with occasional discontinuities when confidence weakens or individual structures break. That is what we mean by the Dodgeball Market where "surprises" are skewed to the downside and investors need to learn to "dodge, dip, duck, dive and...dodge".

In investing, the original sin sits in the initial conditions. In credit, the last decade rewarded speed and deployment and scale. It also rewarded a drift away from old-school credit underwriting, helped along by a self-reinforcing relationship between private credit and private equity.

That drift shows up in three places we keep coming back to: (i) Watered down or non-existent covenants that delay intervention until late in the day. (ii) Leverage masked by “adjusted EBITDA” that makes companies look more profitable than they are. (iii) Documentation and structuring wildly in favour of borrowers that permits value leakage, layering and collateral dilution. Facilities that look senior secured on day one can migrate into HoldCo risk before the first covenants start to bite.

This is the context for our partnership with DunPort and why we published our joint DunPort / Vertis Lower Mid-Market White Paper.

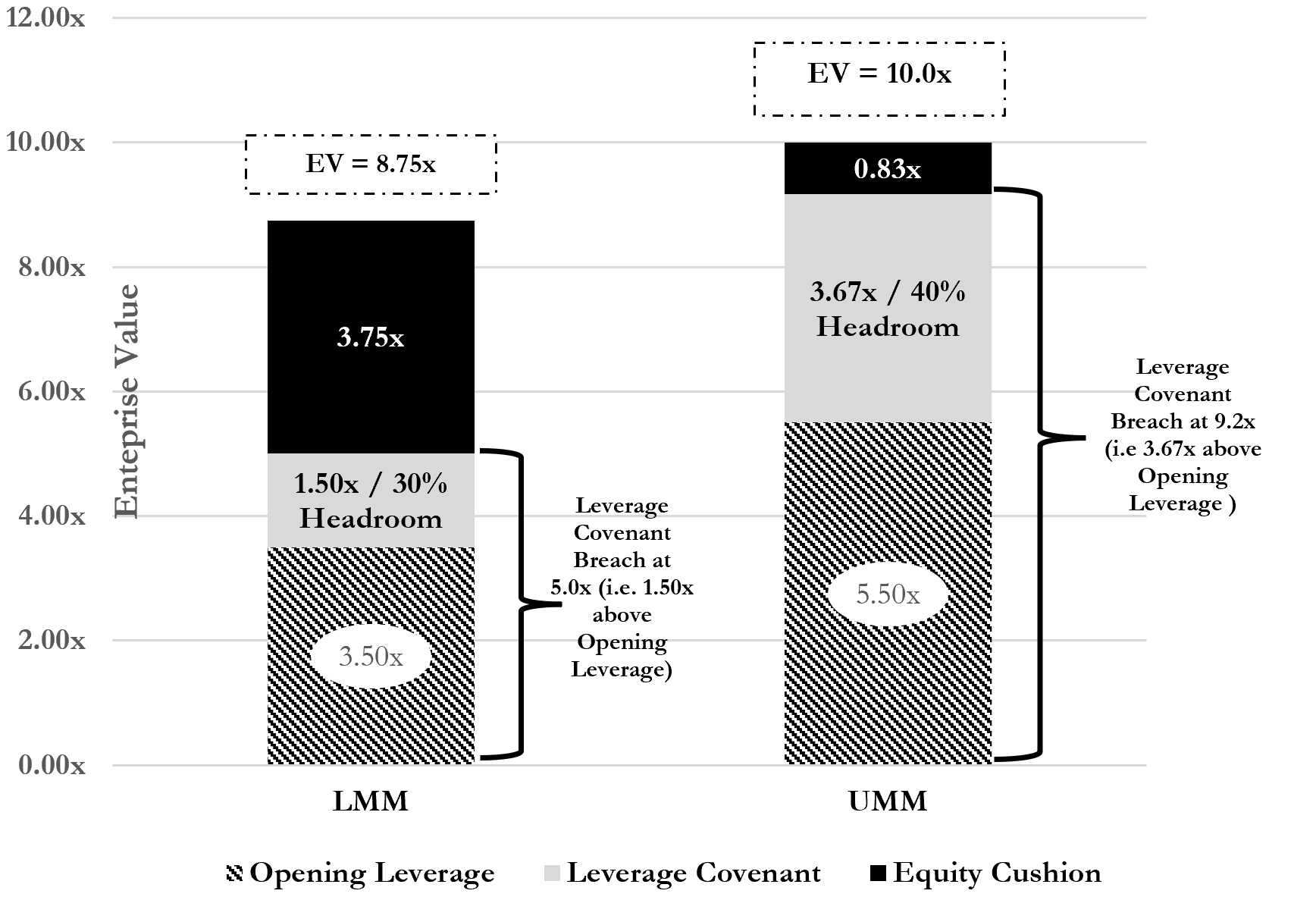

When we say “Lower Mid-Market” (LMM), we mean loan sizes of €/£10m to €/£100m. The point is not company size on its own. The point is the leverage profile, structure and quality of the loan. The structural point matters more than the headline spread. In the LMM, we still expect maintenance covenants, real deleveraging profiles, and structures that allow for pro-active lender conversations.

From a borrower’s perspective, this approach is not punitive. It is protective. Covenants function as an active risk-management tool that supports management while there is still time to adjust course. Lower leverage, combined with clear structure, creates room to manoeuvre. It brings conversations forward, before pressure turns into crisis. In many cases, the excesses of recent years can produce worse outcomes for everyone involved, including management, employees, equity holders, and lenders, than a more disciplined underwriting would have delivered. Our aim is to avoid those outcomes, not profit from them.

The White Paper lays out two pieces of math that frame the opportunity.

First, the default fallacy. We cite S&P/LCD data showing loans under $100m have a roughly three-times lower default rate than loans above $100m. We also cite research indicating leverage is materially more relevant to default risk than borrower size.

Second, the equity cushion. In a typical upper mid-market deal, by the time the leverage covenant finally bites, there may be little equity value left to protect alignment. In the LMM, because leverage is lower and covenants are tighter, there can be meaningful equity value still in the business when the covenant bites. That difference changes behaviour. It brings sponsors and management to the table earlier, while there is still time and an ability to course correct.

Structure drives outcomes. Covenants are the early warning system of the credit investor. In the LMM, that system is still intact.

Read the Full White Paper: “Private Credit: A Case for the Lower Middle-Market”

THREE QUESTIONS FOR:

Vertis: You are one of the veterans in Lower-Mid Market cash-flow lending in Europe. What is the #1 thing most people misunderstand about your business and your market?

Morrow: Most people still underestimate the scale of the opportunity in European lower-mid market cash-flow lending — and how persistent the supply/demand mismatch really is.

There’s a tendency to assume “private credit” is one homogenous market where capital is abundant. In reality, the large-cap end has been heavily competed, while the lower-mid market remains structurally under-served. European SMEs and sponsor-backed businesses still need flexible, reliable financing for buyouts, buy-and-build, refinancings, and growth — but traditional bank balance sheets, regulation, and internal risk constraints mean banks often can’t meet that need at the speed, size, or structure required.

What’s misunderstood is that this isn’t a cyclical gap — it’s structural. It creates an enduring opportunity for lenders who can originate consistently, underwrite properly, and support businesses through volatility. And because deals are smaller and more bespoke, it’s a market where discipline and underwriting skill matter far more than volume.

Vertis: DunPort has deployed over €1.4bn in this segment. What is the "red flag" in a deal that makes you walk away immediately, even if the yield looks good?

Morrow: Our core principle is simple: “return of capital first, return on capital second”. If we can’t get comfortable with what the downside scenario might look like and our prospects of full repayment in such a scenario we won’t do the deal, regardless of yield. The biggest “walk away” red flags usually fall into a few buckets:

Misalignment of stakeholders: not enough true risk capital beneath us, or sponsors/shareholders trying to over-gear the business with limited downside protection. We want real “skin in the game” and sensible behaviour around distributions, leakage, and sponsor support.

Weak financial controls and poor transparency: inconsistent management information, aggressive adjustments, unclear working capital dynamics, or governance that doesn’t match the complexity of the business. If we can’t measure performance reliably, we can’t manage risk.

Fragile credit fundamentals: thin margins, high operating leverage, poor free cash flow conversion, or a business model where a small shock can impair debt service.

Concentration and cyclicality risk without mitigation: heavy reliance on a small number of customers/suppliers, or a demand profile that is highly cyclical — especially when combined with leverage.

We always look at risk-adjusted return — in practical terms, the compensation per unit of leverage and the resilience of cash flows under downside cases. If the downside doesn’t work, we don’t “price it away.”

Vertis: What surprised you most about 2025 and as you look at 2026, what are you most excited about for your business and the market opportunity?

Morrow: What surprised me in 2025 was the resilience of lower-mid market demand in Europe.

Unlike parts of the mid and large-cap market where activity was more stop-start, we saw sustained and growing demand from European LMM private equity firms and SME borrowers. Over the 12 months to December 2025 we reviewed more than €4.5bn of deal flow, the largest 12-month period we’ve seen — and that’s notable given the broader narrative that M&A was muted versus historic levels. In our segment, the need for capital didn’t disappear: businesses still required financing for add-ons, refinancings, and strategic transitions.

2025 also felt like a year where the private credit market started to show more dispersion — the first real signs that underwriting standards and documentation matter, and that not all capital is created equal. When markets get choppier, the difference between disciplined lending and “tourist” capital driven by a need to deploy becomes much more visible.

Looking to 2026, what excites me is that the opportunity set should improve for disciplined managers.

If macro volatility persists and more issues emerge in portfolios across the market, we expect two things to happen: (1) borrowers and sponsors place an even higher premium on dependable capital partners, and (2) pricing, structures, and terms can become more rational — with better lender protections and clearer downside control. In our world, that’s when you can build genuinely durable portfolios: backing good businesses, with sensible leverage, strong information rights, and aligned stakeholders.

So I’m excited about 2026 not because risk disappears — it won’t — but because periods like this tend to reward selectivity, structure, and long-term relationships. That’s exactly where we focus.

Vertis: Thank you, Ross, wishing you and the DunPort team much success in 2026!

To find out more about DunPort Capital Management, click here.

At Vertis we are building the leading financing platform for Europe's Lower Mid-Market. We are doing this across cash-flow lending via our strategic partnership with DunPort Capital Management as well as asset-backed lending via Vertis Capital Solutions.

Published by the Investment Team at Vertis.