Fibre Indigestion

Or: What does 'downside protection' mean in digital infrastructure?

Digital infrastructure - fibre, towers, data centres, fixed wireless - has attracted extraordinary volumes of institutional capital over the past decade, often on the basis that it represents a uniquely defensive asset class. The pitch was intuitive: essential services, recurring revenues, supportive government frameworks.

Vertis does not dispute the underlying logic. In fact, some of us have (in our previous lives) debt-funded emerging Alternative Telecom Networks ("AltNets"). We have directly engaged with more than thirty operators across the UK and continental Europe. We have learned a simple lesson: the asset class is only as defensive as the assumptions beneath it. When those assumptions are wrong - as they have proven to be on take-up rates, competitive intensity, and the timeline to cash flow breakeven - the downside can be severe, and conventional credit metrics offer little protection.

Vertis approaches digital infrastructure through a disciplined lending framework built around interlocking pillars: 1) real replacement costs, 2) path to cash flow breakeven, and 3) refinancing potential.

Each pillar is designed to answer a specific question. But taken together, they constitute what we regard as a structurally sound basis for deploying capital into a sector that remains rich in opportunity - but demands far greater rigour than the market applied during the "go go years" of 2019-2023.

A note on intent: We write the Credit Observer to sharpen our own thinking and to hold ourselves accountable to the standards we set. This article is not a criticism of any specific sector or investment strategy. It is merely a reminder that in times of abundant capital it is easy to get carried away. We welcome feedback and the debate.

Real Replacement Cost as Anchor of Downside Protection

The first question Vertis asks of any digital infrastructure asset is simple: what would it cost to build this from scratch today? Replacement cost is an unglamorous metric that puts both capital expenditure and capital efficiency at the forefront of the equation. After all, G.Network is rumoured to have spent around £300 million in both opex and capex. So was replacement cost £300 million?

In short, no. It appears G.Network continued to spend valuable capital digging their own trenches across the streets of London, while almost all other AltNets used existing infrastructure via Openreach – as soon as it became easier to use at scale – to simply upgrade and install their own equipment. That is a significant difference - in cost base, in efficiency, and ultimately in the value a buyer should be willing to attribute to the resulting asset. Eventually it seems that G.Network got sold for a very small fraction of their invested capital figure.

For a lender like Vertis whose mandate is capital preservation, real replacement cost is foundational - it is the floor below which a rational buyer of distressed assets should not need to go. The discipline this imposes on our investment process is straightforward: we will not lend against a valuation that materially exceeds replacement cost unless there is compelling, evidenced commercial traction to justify the premium.

And of course, replacement cost analysis must always also consider the number of competing networks in any given geography. A fibre network in a street served by one other operator has a different (replacement) value profile from one competing with three others. The competitive intensity directly affects the path to cash flows - which brings us to the second pillar.

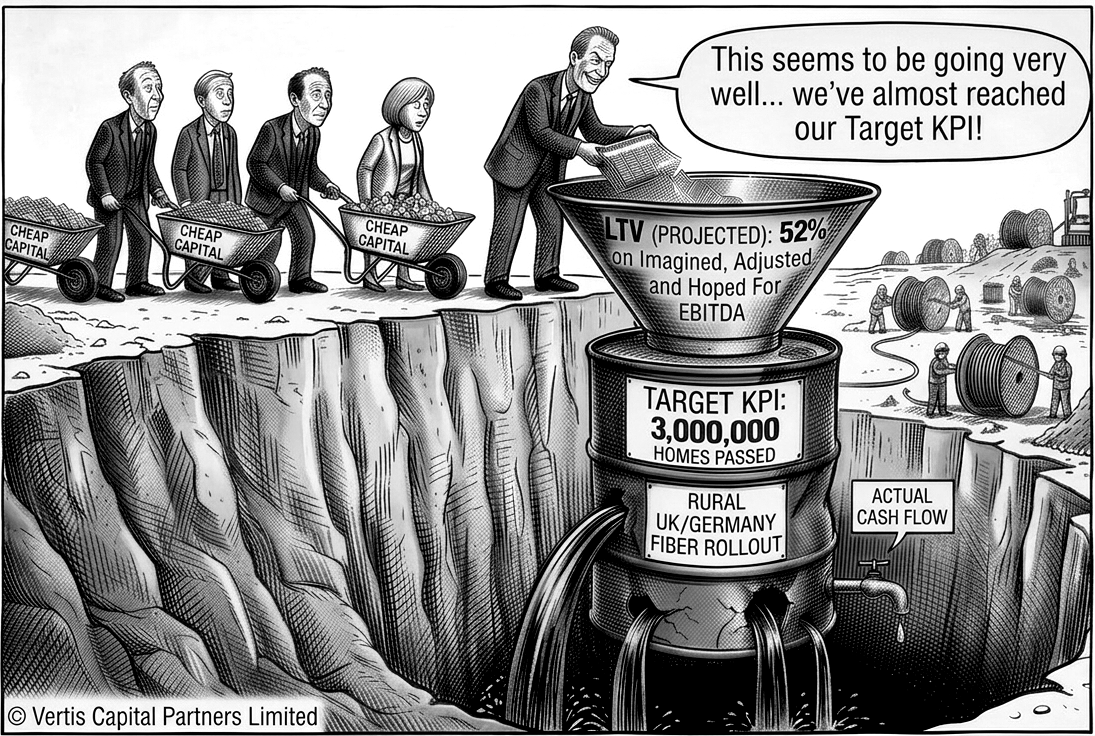

Path to Cash Flow Breakeven: The Question the Industry Avoided

The AltNet investment narrative of 2019 to 2023 was, in retrospect, almost entirely a build story. The metrics that dominated investor presentations - homes passed, network coverage, build rate per quarter - are metrics of deployment, not of commercial viability. Now it is obvious that one needs to build a network first before extracting profits… The point here is that cash flow breakeven, the point at which an operator generates enough revenue from connected customers to cover both its operating costs as well as debt service without further equity injection, was often an afterthought.

The assumption, broadly, was that penetration would come.

It did not come - at least not at the pace or scale that was modelled. And the gap between homes passed and homes connected represents not merely a missed revenue opportunity but an ongoing cash drain: operating costs are broadly fixed against a network footprint, while revenues scale only with actual connections. Every quarter of underperformance against the penetration curve increases capital at risk.

Why does that matter? Because when you lend to a cash-flow negative business, your seniority in the capital structure is theoretical. In practice, your recovery depends entirely on whether you or someone else is willing to fund the business through to cash-flow breakeven. If that funding does not arrive, the business cannot operate, the asset deteriorates, and you quickly realise your asset comes with a liability attached. In that scenario, senior secured recoveries could be quite low.

Vertis therefore requires a credible, independently stress-tested path to cash flow breakeven as a precondition for investment. Cost base, Average Revenue Per User assumptions, competitive overlap, and a minimum penetration rate all come into play. We then assess the probability of reaching that level within a defined timeframe.

And finally, it doesn’t stop here… because the above only deals with the point of “entry” when analysing a credit. We then look at the exit / refinancing potential (or risk).

Refinancing Potential: Stress-Testing the Capital Structure

Digital infrastructure assets are, by nature, capital-intensive and slow to generate returns. The period between initial deployment and sustainable cash generation can span many years, and the capital structures used to finance that period must be stress-tested not merely against a base case, but against a realistic downside.

The question Vertis asks here is whether the capital structure can be refinanced at maturity on terms that do not require either a forced sale or a distressed equity injection.

This matters because a significant proportion of the UK AltNet sector entered 2025 and 2026 facing refinancing walls at exactly the moment when lender appetite for the sector had contracted sharply.

Institutions that had extended credit based on projected penetration rates that never materialised found themselves holding loans against assets with far weaker cash flows than underwritten. The refinancing risk was not hidden - it was present in every structure from the outset - but it was frequently underweighted in the optimism of the build phase.

Digital infrastructure assets have historically traded at premium multiples - 15 to 20x Forward EBITDA in mature, cash-generative networks with strong market positions. Those multiples were extrapolated into the valuation of early-stage AltNets that had passed hundreds of thousands of homes but connected a fraction of them. The implicit assumption was that penetration would normalise, EBITDA would scale, and the multiple would hold. The AltNet “distress” cycle of 2024 to 2026 has been, in large part, the market correcting for that category error.

Vertis models what the asset will look like at the point of debt maturity under a range of penetration assumptions - including scenarios materially below management's base case - and we ask whether, at those levels, a credible lender universe exists and at what leverage multiple. If the answer requires a heroic set of commercial assumptions to reach a refinanceable position, we view that as a structural flaw in the investment case, not a risk to be mitigated through covenant protection alone.

These three pillars are not independent. Replacement cost anchors the downside, the breakeven path defines the commercial risk and the refinancing analysis stress-tests the structure. An investment that passes all three tests is, in our view, a genuinely defensible opportunity in a sector that has demonstrated an uncanny ability to create and destroy value at scale - with those disciplines being the deciding factor.

And of course, a few distressed companies clearly do not make a failed sector. Digital infrastructure remains rich with defensible, high-quality debt opportunities - and we are actively assessing several. And having learned from this cycle, we will be even more disciplined when we do.

NINE QUESTIONS FOR: JEREMY CHELOT

Chief Executive Officer, Netomnia and YouFibre.

In February 2026, Netomnia was sold for approximately £2 billion to a consortium led by Telefónica, Liberty Global and InfraVia Capital, pending clearance from the Competition and Markets Authority. As we described above, against a backdrop of distress across the UK AltNet sector, the transaction stands as one of the few success stories of the cycle.

We interviewed the CEO of Netomnia and YouFibre, Jeremy Chelot, about his views on “what went wrong for the sector”, valuation metrics, the funding environment and consolidation. The views expressed in here are solely his own.

Vertis: Let us start with Netomnia and our lending lens. Based on public filings, Netomnia has close to £1.2 billion of gross debt, including £300 million of mezzanine raised in September 2025 - against reported FY2025 EBITDA of just £5 million. For a lender focused on downside protection and capital preservation, those Debt/EBITDA ratios go far beyond anything conventional credit metrics would support. Help us bridge the gap in that thought process.

Chelot: We raised infrastructure debt from commercial banks for the first time in 2023, so we are only three years into a seven-year facility. That context matters. We have consistently outperformed the plans we set with our lenders. While these plans remain under close review with our board, we consider it possible to achieve leverage below 4x EBITDA by the time our debt facility matures.

Vertis: In hindsight, for the lenders who funded the AltNet buildout, what do you think they should have done differently in terms of structuring, monitoring, and covenant design? Or, were they just not able to set terms because so much capital was chasing the same opportunity?

Chelot: One metric should have been non-negotiable from day one: Net Debt to Premises Connected. Too many facilities were structured with draw stops over the first five years, without sufficient linkage to actual commercial performance. That disconnect has proven problematic. We did not have that structure ourselves.

Vertis: The debate around Homes Passed versus Homes Connected has been central to the industry's reckoning. A few years ago, every AltNet we met - Netomnia included - was primarily focused on build rates. That has now completely flipped, and monetisation has taken centre stage. But is this a case of 'too little, too late' for penetration rates to recover, or is it simply the normal course of business - build first, then commercialise?

Chelot: I push back on the premise. Capital providers, both equity and debt, have always focused on take-up. I haven't met a credible CEO in this sector who wasn't focused on penetration from day one. The sequence is not a failure of priorities; it is a physical reality, you cannot monetise a network you have not built. Where I do agree is that industry penetration targets were often too aggressive. We have always underwritten to a maximum of 33% take-up, and that discipline is important.

Vertis: Over the last six years, the senior partners at Vertis have met more than thirty AltNet operators. Almost without exception, their original business plans showed 30% penetration within three to five years. Today, most are at best half of that metric. At a high level, what do you think went wrong?

Chelot: When we did our first debt deal in 2021, we committed to 33% penetration over five years. Every cohort has delivered that in five years or less, so the target is achievable. But three years is not. With national churn at around 15%, you are competing for a limited pool of switching customers, and winning a disproportionate share of that takes time.

Vertis: G.Network is rumoured to have been sold for a fraction of the capital invested in it, while Gigaclear is rumoured to be facing restructuring. Beyond the headline of low take-up rates, are there specific lessons from those cases - decisions made, assumptions held, structures chosen - that the rest of the industry has not yet fully internalised?

Chelot: Three clear lessons. First, do not build your own infrastructure when competing against operators using Openreach’s PIA; it is significantly more expensive and materially slower. Second, there is no valuation premium for avoiding PIA. Third, prioritise retail; it is a more dynamic market with less inertia than B2B.

Vertis: Capital was relatively abundant over the past decade, and that abundance arguably made capital efficiency an afterthought - leading to more than several competing networks per household in parts of the country. On that basis, going forward, what does “disciplined capital deployment” actually look like in this sector now?

Chelot: The industry has already deployed most of the capital. Very few Alt-Nets in the UK are still actively building at scale, and even those that are have slowed materially. The focus now must be on monetisation, driving penetration and reaching cash flow breakeven as quickly as possible. That is what disciplined capital allocation looks like today.

Vertis: The Netomnia sale will inevitably become the valuation reference point against which every other AltNet in the market is benchmarked. What implications do you think that transaction will have on valuation expectations across the industry, particularly for operators who are nowhere near Netomnia's scale or commercial traction?

Chelot: It sets a benchmark, but it needs to be understood in context. We exited well before reaching peak penetration, ARPU, EBITDA, and free cash flow. The valuation reflects future potential, not a fully matured asset.

Vertis: Consolidation has been described as 'inevitable' for three consecutive years and has still not happened at scale. Is the real problem simply that sellers will not accept what their networks are actually worth today?

Chelot: Two problems, not one. The first is valuation expectations; sellers are still anchored to levels that do not reflect where we are in the cycle. The second is liquidity. There is very little cash available in the market, which makes large-scale transactions, particularly all-share mergers, difficult to execute. Until one of those shifts, consolidation will remain more talked about than done.

Vertis: At what point does a wave of AltNet collapses become a systemic risk to the UK's digital infrastructure ambitions - i.e. not just a private capital problem, but a national one? And if the government's gigabit coverage goals were genuinely the priority, wouldn't a single well-regulated open-access wholesale network have served the country better than fifty-plus competing operators burning through investor capital in the same streets?

Chelot: The infrastructure is already built, so the systemic risk is minimal. The real question is how consolidation plays out. Will it create scaled challengers to Openreach, or will the market remain structurally similar, with competition concentrated at the retail level and limited wholesale disruption?

Vertis: Thank you, Jeremy, wishing you all the best with closing the transaction and future endeavours.

The views expressed in this interview are solely those of Jeremy Chelot in his personal capacity and do not represent the views of Netomnia, its shareholders, or any other party. This document has been prepared for informational purposes only and does not constitute investment advice or a solicitation to invest.

At Vertis we are building the leading financing platform for Europe's Lower Mid-Market. We are doing this across cash-flow lending via our strategic partnership with DunPort Capital Management as well as asset-backed lending via Vertis Capital Solutions.

Published by the Investment Team at Vertis.